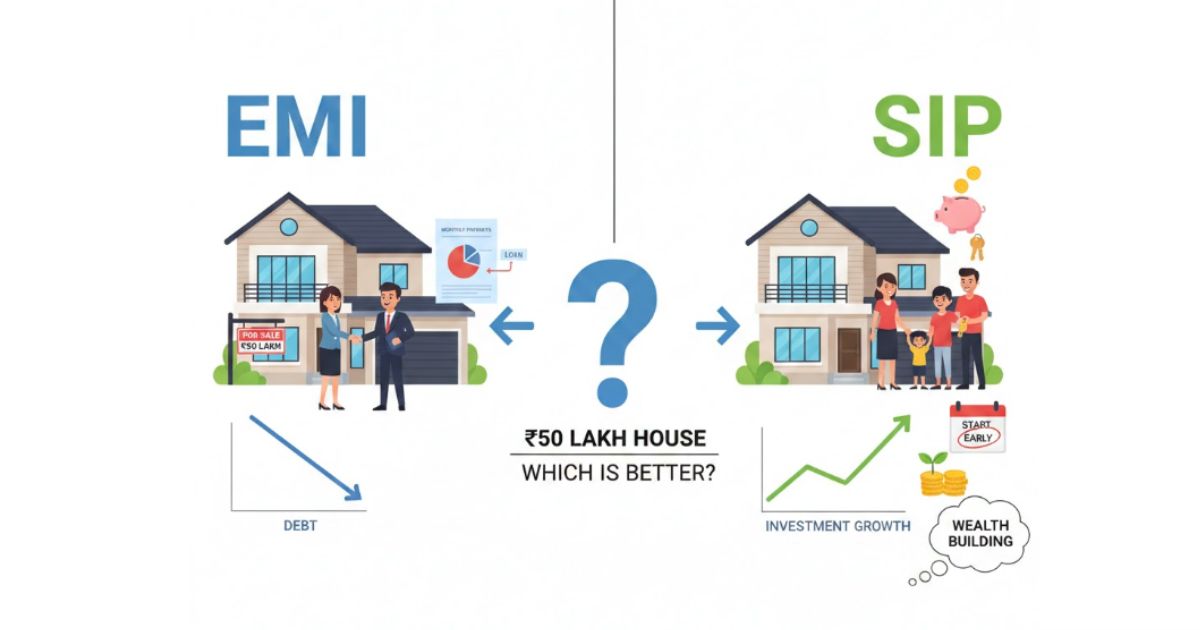

EMI vs SIP: Which Is Better to Buy a ₹50 Lakh House?

EMI vs SIP for a house: Buying a house is one of the most significant dreams for many people. However, rising property prices and long-term loan commitments make this decision financially challenging. Because of this, many people are confused between taking a home loan and paying EMI or investing the same amount through SIP and buying a house later.

Let’s understand both options with clear calculations.

Home Loan EMI for a ₹50 Lakh House

If you take a home loan of ₹50 lakh at an interest rate of 7.9% for 20 years, here’s what the numbers look like:

Monthly EMI: ₹41,511

Total amount paid in 20 years: ₹99,62,727

Total interest paid: ₹49,62,727

This means the interest alone is almost equal to the loan amount. While a home loan helps you buy a house immediately, it also becomes a long-term financial burden.

Advantages of Home Loan EMI

Immediate home ownership

No need to pay rent

Emotional and family security

Tax benefits on home loan interest and principal

Disadvantages of Home Loan EMI

High interest cost

Long-term financial pressure

Less flexibility for other investments

SIP Investment Instead of EMI: What If You Invest ₹41,500 Monthly?

Now consider investing the same ₹41,500 per month in a mutual fund SIP for 20 years, assuming an average return of 12% per annum.

Total investment: ₹99,60,000

Estimated returns: ₹3,15,04,638

Total corpus after 20 years: ₹4,14,64,638

This is more than four times the invested amount. With disciplined investing, you may be able to accumulate ₹50 lakh within 7 years, depending on market performance.

Advantages of SIP

Strong compounding over the long term

Potentially higher returns than real estate

Better liquidity

Helps beat inflation

Risks of SIP

Market volatility

No guaranteed returns

Requires patience and discipline

Delayed house ownership

EMI vs SIP: Which Option Is Better?

The right choice depends on several factors:

Real estate price appreciation

Inflation and cost of living

Rental expenses

Market risks in mutual funds

Income stability and risk tolerance

A house worth ₹50 lakh today may cost significantly more after 20 years. At the same time, SIP returns depend on market conditions and cannot be predicted with certainty.

Frequently Asked Questions (FAQ)

Is SIP better than EMI for buying a house?

SIP can generate higher wealth in the long run, but EMI offers immediate home ownership. The choice depends on your financial goals.

Can SIP really grow to over ₹4 crore in 20 years?

At an average 12% return, yes. However, mutual fund returns are market-linked and not guaranteed.

Is delaying house purchase risky?

Yes. Property prices and rents may increase, affecting affordability in the future.

Should I consult a financial advisor before deciding?

Yes. A certified financial advisor can help you choose the best strategy based on your income and goals.

Conclusion

There is no single correct answer in the EMI vs SIP debate.

If owning a home immediately is your priority, a home loan EMI may be suitable.

If long-term wealth creation and flexibility matter more, SIP investing can be a powerful alternative.

A balanced financial plan that considers both real estate and investments is often the smartest approach.

Disclaimer: This article is for informational purposes only. Market investments are subject to risk. Please consult a financial expert before making investment decisions.

- US-Iran Talks Begin as Hormuz Tensions Shake Oil Markets - April 11, 2026

- Iran’s New Supreme Leader Reportedly Recovering from Serious War Injuries - April 11, 2026

- EU Airline Industry Warns of Fuel Shortages if Strait of Hormuz Stays Closed - April 11, 2026